One tactic is sanctioning, which applies economic restrictions on a country’s government, businesses, and even individual citizens. In theory, these penalties create enough impact to dissuade further hostility. Today, the U.S. maintains more sanctions than any other country, and one of its most comprehensive programs is aimed at Russia. To learn more, we’ve compiled an overview of these sanctions using data from the Congressional Research Service and U.S. Treasury.

Sanctions by Catalyst Event

Sanctions are often introduced after a President issues an executive order (EO) that declares a national emergency. This provides special powers to regulate commerce with an aggressor nation. Our starting point will be Russia’s 2014 invasion of Ukraine, as this is where a majority of ongoing sanctions have originated.

Catalyst: 2014 Ukraine Invasion

On March 18, 2014, Russia annexed Crimea from Ukraine. This was denounced by the U.S. and its allies, leading them to impose wide-reaching sanctions. President Obama’s EOs are listed below. Altogether, these sanctions affect 480 entities (includes businesses and government agencies), 253 individuals, 7 vessels, and 3 aircraft. Sanctions against ships and planes may seem odd, but these assets are often owned by sanctioned entities. For example, in February 2022, France seized a cargo ship belonging to a sanctioned Russian bank.

Catalyst: U.S. Election Interference

The Obama, Trump, and Biden administrations have all imposed sanctions against Russia for its malicious cyber activities. Altogether, these sanctions affect 106 entites, 136 individuals, 6 aircraft, and 2 vessels. A critical target is the Internet Research Agency (IRA), a Russian company notorious for its online influence operations. Prior to the 2016 election, 3,000 IRA-sponsored ads reached up to 10 million Americans on Facebook. This problem escalated in the run-up to the 2020 election, with 140 million Americans being exposed to propaganda on a monthly basis.

Catalyst: Various Geopolitical Dealings

The U.S. maintains various sanctions designed to counteract Russian influence in Syria, Venezuela, and North Korea. *These are recent sanctions pursuant to EOs that were issued many years prior. For example, EO 13582 was introduced in August 2011. These sanctions impact 23 entities, 17 individuals, and 7 vessels. Specific entities include Rosoboronexport, a state-owned arms exporter which was sanctioned for supplying the Syrian government. As of December 2020, Syria’s government was responsible for the deaths of 156,329 people (civilians and combatants) in the civil war.

Catalyst: Chemical Poisonings of Individuals

The Russian government has been accused of poisoning two individuals in recent years. The first incident involved Sergei Skripal, a former Russian intelligence officer who was allegedly poisoned in March 2018 on UK soil. The second, Alexei Navalny, a Russian opposition leader, was allegedly poisoned in August 2020. The Chemical and Biological Weapons Control and Warfare Elimination Act of 1991 (CBW Act) allows sanctions against foreign governments that use chemical weapons. Nine individuals and five entities were sanctioned as a result of the two cases.

Catalyst: 2022 Ukraine Invasion

The U.S. has introduced many more sanctions in response to Russia’s latest invasion of Ukraine. EO 14024, which was issued in February 2022, targets Russia’s major financial institutions and their subsidiaries (83 entities in total). Included in this list are the country’s two largest banks, Sberbank and VTB Bank. Together, they hold more than half of all Russian banking assets. Also targeted are 13 private and state-owned companies deemed to be critical to the Russian economy. Included in this 13 are Rostelecom, Russia’s largest digital services provider, and Alrosa, the world’s largest diamond mining company.

Do Sanctions Work?

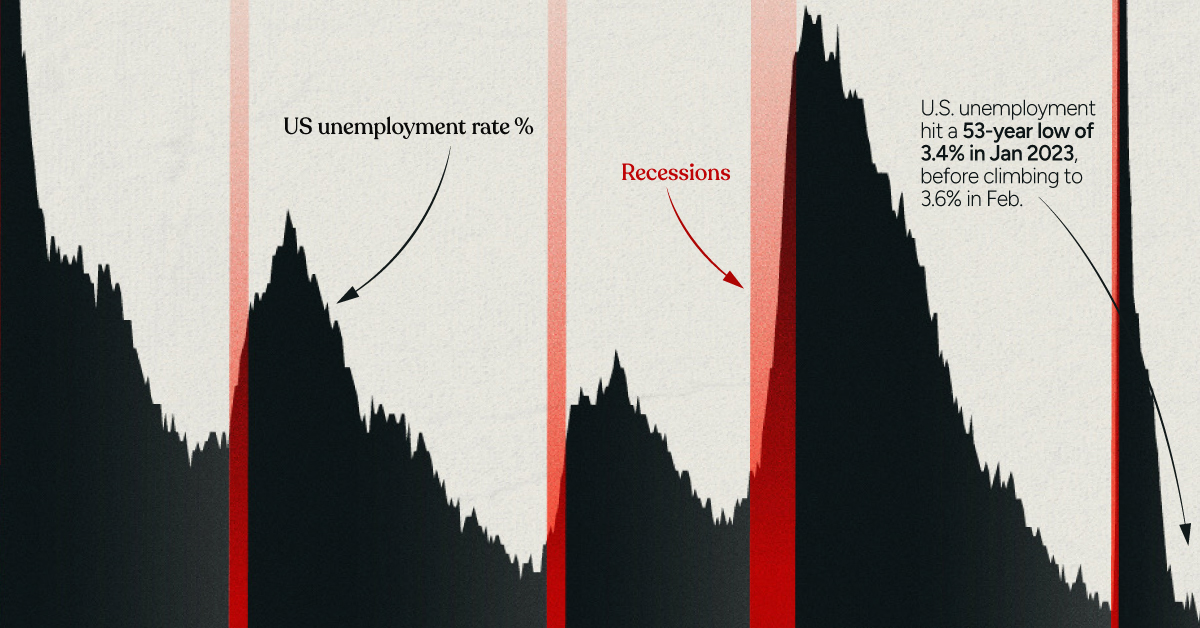

Proving that a sanction was solely responsible for an outcome is impossible, though there have been successes in the past. For example, many agree that sanctions played an important role in ending Libya’s weapons of mass destruction programs. Critics of sanctions argue that imposing economic distress on a country can lead to unintended consequences. One of these is a shift away from the U.S. financial system. In other words, sanctions can create an impact as long as the U.S. dollar continues to reign supreme. on Both figures surpassed analyst expectations by a wide margin, and in January, the unemployment rate hit a 53-year low of 3.4%. With the recent release of February’s numbers, unemployment is now reported at a slightly higher 3.6%. A low unemployment rate is a classic sign of a strong economy. However, as this visualization shows, unemployment often reaches a cyclical low point right before a recession materializes.

Reasons for the Trend

In an interview regarding the January jobs data, U.S. Treasury Secretary Janet Yellen made a bold statement: While there’s nothing wrong with this assessment, the trend we’ve highlighted suggests that Yellen may need to backtrack in the near future. So why do recessions tend to begin after unemployment bottoms out?

The Economic Cycle

The economic cycle refers to the economy’s natural tendency to fluctuate between periods of growth and recession. This can be thought of similarly to the four seasons in a year. An economy expands (spring), reaches a peak (summer), begins to contract (fall), then hits a trough (winter). With this in mind, it’s reasonable to assume that a cyclical low in the unemployment rate (peak employment) is simply a sign that the economy has reached a high point.

Monetary Policy

During periods of low unemployment, employers may have a harder time finding workers. This forces them to offer higher wages, which can contribute to inflation. For context, consider the labor shortage that emerged following the COVID-19 pandemic. We can see that U.S. wage growth (represented by a three-month moving average) has climbed substantially, and has held above 6% since March 2022. The Federal Reserve, whose mandate is to ensure price stability, will take measures to prevent inflation from climbing too far. In practice, this involves raising interest rates, which makes borrowing more expensive and dampens economic activity. Companies are less likely to expand, reducing investment and cutting jobs. Consumers, on the other hand, reduce the amount of large purchases they make. Because of these reactions, some believe that aggressive rate hikes by the Fed can either cause a recession, or make them worse. This is supported by recent research, which found that since 1950, central banks have been unable to slow inflation without a recession occurring shortly after.

Politicians Clash With Economists

The Fed has raised interest rates at an unprecedented pace since March 2022 to combat high inflation. More recently, Fed Chairman Jerome Powell warned that interest rates could be raised even higher than originally expected if inflation continues above target. Senator Elizabeth Warren expressed concern that this would cost Americans their jobs, and ultimately, cause a recession. Powell remains committed to bringing down inflation, but with the recent failures of Silicon Valley Bank and Signature Bank, some analysts believe there could be a pause coming in interest rate hikes. Editor’s note: just after publication of this article, it was confirmed that U.S. interest rates were hiked by 25 basis points (bps) by the Federal Reserve.