Modern credit systems are now powered by sophisticated algorithmic credit scoring, the use of trended and alternative data, and innovative fintech applications. While these developments are all interesting in their own right, together they serve as a technological foundation for a much more profound shift in consumer credit in the coming years.

The Future of Consumer Credit

In today’s infographic from Equifax, we look at the cutting edge of consumer credit, including the new technologies and global trends that are shaping the future of how consumers around the world will access credit. It’s the final piece of our three-part series covering the past, present, and future of credit.

The biggest problem that creditors have always faced is well-documented. There is more to a borrower than just their credit score. Yet creditors do not always have a 360 degree view of a consumer’s creditworthiness in order to better assess their overall score. Called “information asymmetry”, this gap has gotten smaller over the years thanks to advancements in technology and business practices. However, it still persists in particular situations, like when a college student has no credit history, or when a rural farmer in India wants to take out a loan to buy seeds for crops. But thanks to growing amounts of data – as well as the technology to make use of that data – high levels of information asymmetry may soon be a thing of the past.

Forces Shaping Credit’s Future

Here are some of the major forces that will drive the future of consumer credit, addressing the information asymmetry problem and making a wide variety of credit products available to the public:

- Growing Data 90% of the data in all of human history has been created in just the last two years.

- Changing Regulatory Landscape New international regulations are putting personal data back in the hands of consumers, who can control the personal data they authorize access to.

- Game-changing Technologies Machine learning, deep learning, and neural networks are giving companies a way to garner insights from data.

- Focus on Identity Authenticating the identity of consumers will become crucial as credit becomes increasingly digital. Blockchain and biometrics could play a role.

- The Fintech Boom The democratization of data and tech is allowing small and niche players to come in and offer new, innovative products to consumers.

The Credit Revolution

No one can predict the future, but the above forces are shaping the credit industry to be a very different experience for consumers and businesses. Here are how things could change.

More Data, New Models

Current credit scoring algorithms use logistical regressions to compute scores, but these really max out at using 30-50 variables. In addition, these models can’t “learn” new things like AI can. However, with new technologies and an unprecedented explosion in data taking place, it means that this noise can be converted into insights that could help increase trust in the credit marketplace. New algorithms will be multivariate, and they will be able to mine, structure, weight, and use this treasure trove of data. Neural networks will be able to look at a billions of data points to find and make sense of extremely rare patterns. They will also be able to explain why a particular decision was made – and at a time where transparency is crucial, this will be key.

Data Will be in the Hands of Consumers

Today, much of consumers’ financial data – such as loan repayment histories – is held almost exclusively by banks and credit agencies. However, tomorrow points to a very different paradigm: much of the data will be directly in the hands of consumers. In other words, consumers will be able to decide how their data gets used, and for what. In Europe, changes have already been made to transfer control of personal data to the consumer, such as the PSD2, GDPR, and Open Banking (U.K.) initiatives. Experts see the trend towards open data growing globally, and eventually reaching the United States. Open data will allow consumers to:

Regain control of checking, mortgage, loan, and credit card data Give up more information voluntarily to unlock better deals from creditors Grant access to third parties (fintech, apps, etc.) to use this data in new applications and products Gain access to better rates, new lending models, and more

Identity Will Be Just as Important

As transactions become more digital and remote, how lenders verify the identity of borrowers will be just as important as the lending data itself. Why? Credit is based around trust – and fraud is the biggest risk for lenders. But fraud an be prevented by new technologies that help detect anomalies and prove a borrower’s identity: Blockchain Distributed, tamper-resistant databases can help secure people’s identities from fraudulent activity Biometrics Fingerprints, facial recognition, and other biometric identification schemes could help secure identities as well

New Game, New Players

With the vast expansion in types and volume credit data, new technologies, and standardized data in the hands of consumers, there will be a new era of third-party companies and apps that can provide useful and relevant services for consumers. Here are just some emerging fields in lending: In the future, consumers may not have to even request credit – it may be automatically allocated to them based on behavior, age, assets, and needs. Consumers will have more control, and more options than ever before.

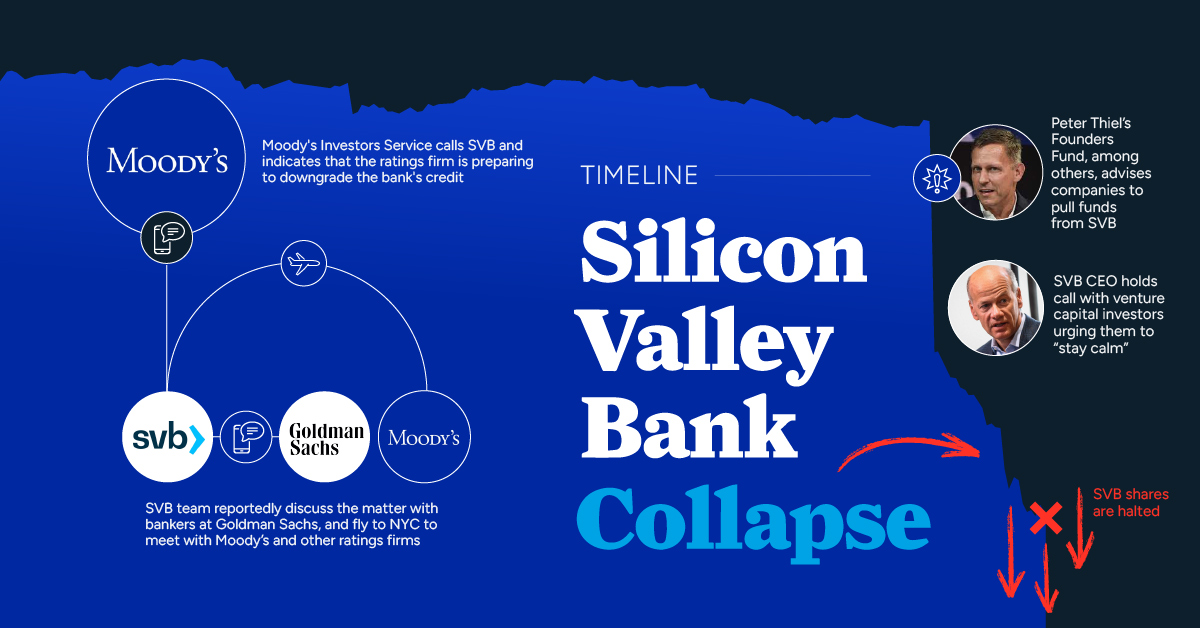

on But fast forward to the end of last week, and SVB was shuttered by regulators after a panic-induced bank run. So, how exactly did this happen? We dig in below.

Road to a Bank Run

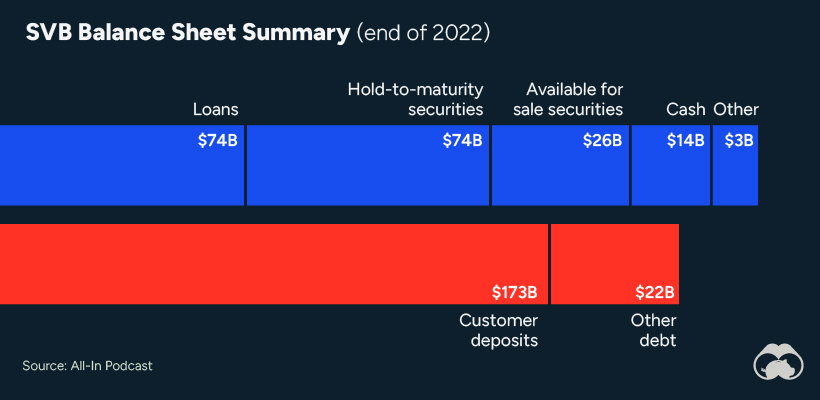

SVB and its customers generally thrived during the low interest rate era, but as rates rose, SVB found itself more exposed to risk than a typical bank. Even so, at the end of 2022, the bank’s balance sheet showed no cause for alarm.

As well, the bank was viewed positively in a number of places. Most Wall Street analyst ratings were overwhelmingly positive on the bank’s stock, and Forbes had just added the bank to its Financial All-Stars list. Outward signs of trouble emerged on Wednesday, March 8th, when SVB surprised investors with news that the bank needed to raise more than $2 billion to shore up its balance sheet. The reaction from prominent venture capitalists was not positive, with Coatue Management, Union Square Ventures, and Peter Thiel’s Founders Fund moving to limit exposure to the 40-year-old bank. The influence of these firms is believed to have added fuel to the fire, and a bank run ensued. Also influencing decision making was the fact that SVB had the highest percentage of uninsured domestic deposits of all big banks. These totaled nearly $152 billion, or about 97% of all deposits. By the end of the day, customers had tried to withdraw $42 billion in deposits.

What Triggered the SVB Collapse?

While the collapse of SVB took place over the course of 44 hours, its roots trace back to the early pandemic years. In 2021, U.S. venture capital-backed companies raised a record $330 billion—double the amount seen in 2020. At the time, interest rates were at rock-bottom levels to help buoy the economy. Matt Levine sums up the situation well: “When interest rates are low everywhere, a dollar in 20 years is about as good as a dollar today, so a startup whose business model is “we will lose money for a decade building artificial intelligence, and then rake in lots of money in the far future” sounds pretty good. When interest rates are higher, a dollar today is better than a dollar tomorrow, so investors want cash flows. When interest rates were low for a long time, and suddenly become high, all the money that was rushing to your customers is suddenly cut off.” Source: Pitchbook Why is this important? During this time, SVB received billions of dollars from these venture-backed clients. In one year alone, their deposits increased 100%. They took these funds and invested them in longer-term bonds. As a result, this created a dangerous trap as the company expected rates would remain low. During this time, SVB invested in bonds at the top of the market. As interest rates rose higher and bond prices declined, SVB started taking major losses on their long-term bond holdings.

Losses Fueling a Liquidity Crunch

When SVB reported its fourth quarter results in early 2023, Moody’s Investor Service, a credit rating agency took notice. In early March, it said that SVB was at high risk for a downgrade due to its significant unrealized losses. In response, SVB looked to sell $2 billion of its investments at a loss to help boost liquidity for its struggling balance sheet. Soon, more hedge funds and venture investors realized SVB could be on thin ice. Depositors withdrew funds in droves, spurring a liquidity squeeze and prompting California regulators and the FDIC to step in and shut down the bank.

What Happens Now?

While much of SVB’s activity was focused on the tech sector, the bank’s shocking collapse has rattled a financial sector that is already on edge.

The four biggest U.S. banks lost a combined $52 billion the day before the SVB collapse. On Friday, other banking stocks saw double-digit drops, including Signature Bank (-23%), First Republic (-15%), and Silvergate Capital (-11%).

Source: Morningstar Direct. *Represents March 9 data, trading halted on March 10.

When the dust settles, it’s hard to predict the ripple effects that will emerge from this dramatic event. For investors, the Secretary of the Treasury Janet Yellen announced confidence in the banking system remaining resilient, noting that regulators have the proper tools in response to the issue.

But others have seen trouble brewing as far back as 2020 (or earlier) when commercial banking assets were skyrocketing and banks were buying bonds when rates were low.