But while the speed of order executions are infinitely more impressive across the board, the conceptual backbone behind the stock market itself hasn’t changed much. In fact, the model we use today for settling trades and ensuring proper share ownership is still based on the one initially created in the 17th Century.

A Decentralization of Equities?

Today’s infographic comes to us from Equibit, and it envisions what a decentralized securities platform could look like. In such a paradigm, the settlement of trades would not occur through centralized transfer agents, but instead through a blockchain with this feature “built in”. The application of blockchain technology could take the modernization of the stock market one step further. Instead of technology being used simply to speed up more complex transactions, the blockchain could change how the plumbing behind the system works to mitigate current risks and problems. But to understand how transformative this idea is, we need to look at the history behind the current model first.

The Roots of the Modern Market

The roots of the modern stock market can be traced back to Amsterdam in the year 1602, when the Dutch East India Company became the world’s first “publicly traded” company. Trade missions to the West Indies were risky and expensive – so shares and bonds in the company were initially sold to a large pool of interested investors to spread the risk. In turn, backers of the company received a guarantee of some future share of profits. As investors began speculating about the prospects of the Dutch East India Company, a secondary market quickly developed for these securities. People bought and sold stock in high volumes, and a central registrar tracked the transfer of shares between parties.

The Backbone of Today’s Market

Over 400 years later, the stock market is not that much different from the earliest exchange found in Amsterdam. Modern computing and the internet have sped up transactions so they can be executed in milliseconds, but the conceptual backbone of the market hasn’t changed at all. Stock Transfer Agents are the centralized registrars in the background that track share ownership for issuers and the stock market. They are a third party that will cancel the share certificate for the investor that sold the shares, and substitute the new owner’s name on the official master shareholder listing. There are over 130 stock transfer agents in the USA and Canada, maintaining the records of more than 100 million shareholders on behalf of over 15,000 issuers.

New Technology, Old Model

While modern stock transfer agents use today’s technology, the same old model persists – and it creates multiple industry problems: Centralized and expensive

Depositories and transfer agents are a single point of failure Registration, transfer, distribution, scrutineering, courier fees The more widely held, the higher the administration costs

Limited Transparency

Information asymmetry leads to market advantages Forged securities still a concern Counterparty risk is systemic

Furthermore, legal ownership rests with transfer agents in most jurisdictions. Investors actually do not have title. At the same time, the industry is huge – just one company, The Depository Trust & Clearing Corporation (DTCC) is the highest financial value processor in the world with $1.6 quadrillion in transactions in 2016.

The Problem With Centralization

During the Financial Crisis, the problems of increased centralization and limited transparency reared their ugly head. Companies like Lehman Brothers and MF Global self-destructed – and nobody knew what kind of assets they had off their balance sheets. – J. Christopher Giancarlo, Commodity Futures Trading Commission This lack of clarity and risk helped drive hysteria, ultimately exacerbating the extent of the crisis. Because no one could quantify the risks, investors liquidated their assets. More selling meant even less liquidity.

Enter the Blockchain

Instead of putting all stock transactions through a centralized hub, the blockchain can be used to directly transfer share ownership between investors.

Here’s how a decentralized securities platform could work:

In other words, stock exchanges could run using a blockchain under the hood, with no longer any need for a centralized settlement or transfer of share certificates.

This is cheaper, faster, reduces risks, and more secure. It also would be fully transparent.

Even better, such a platform could also serve as the base for other value adds – and fully transform the way we think about equity markets.

on

For a modern example, we can see how different countries (and regions) act when it comes to cryptocurrency. Within the European Union—one of the regions dealing with faster crypto adoption—attitudes towards investing can vary considerably.

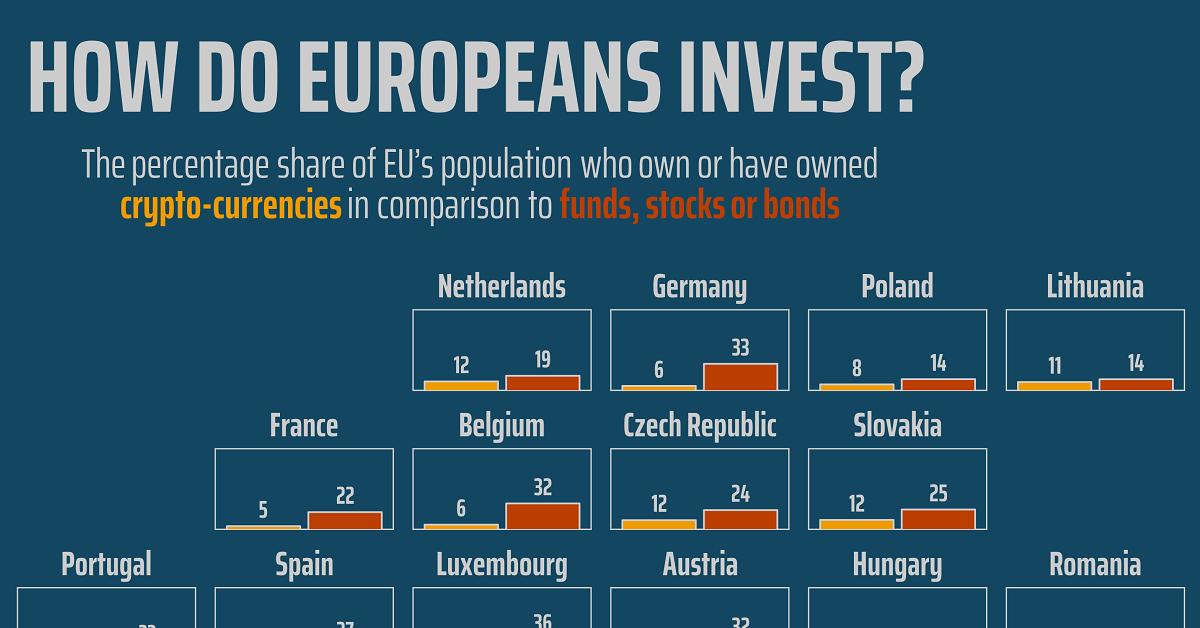

This graphic from Gilbert Fontana looks at crypto popularity amongst investors in the EU using data from the European Commission’s Eurobarometer. It compares exposure to cryptocurrencies relative to stocks, funds, and bonds.

Crypto Popularity in Europe in 2022

Given that crypto has experienced bubble-like asset rallies, including a dramatic rise to over a trillion dollars in value before crashing, it’s fair to say it’s well known by now. But even with a vast rise in awareness, there are still discrepancies between the level of investment crypto receives amongst European Union nations. Let’s see which countries have the highest proportion of citizens invested in crypto: Topping the list is Slovenia, considered by some the most crypto-friendly nation in the world. According to the survey, 18% of the country’s population has some sort of investment in it. Cyprus also ranks high in its crypto-friendly rank and hits an investment figure of 13%. Also notable is the Grand Duchy of Luxembourg, which despite having a small population of 640,000 also has a strong reputation as a global financial hub. When it comes to crypto, 14% of the population owns or has owned the asset, relative to 36% for stocks, bonds, or funds.

Crypto Unpopularity?

In regards to the countries with lower levels of crypto investment, one observation is that they tend to be wealthier and more developed EU nations. Here’s how the nations at or below the 10% crypto-investment threshold rank: At the “bottom” of crypto interest are France, Germany and Italy, also the EU’s largest economies. At a glance, this might suggest that citizens of stronger economies invest less in crypto. However, it’s important to note that the countries with higher levels of crypto investment tend to have lower levels of wealth on average. Though less of their investors seem to engage in crypto trading, countries like France and Germany might have more comparable levels of crypto investment on a pure dollar-basis.