Like many other things in this world, the amount of freedom that people have ebbs and flows with time. In general, it can be argued that political and economic freedoms have been increasing steadily since The Enlightenment – but of course, there are always shorter corrections along the way where freedom seems to spiral downwards in the interim. Right now, we’re in one of those ruts, and global freedom has consecutively declined for a 12 year period.

Democracy in Crisis

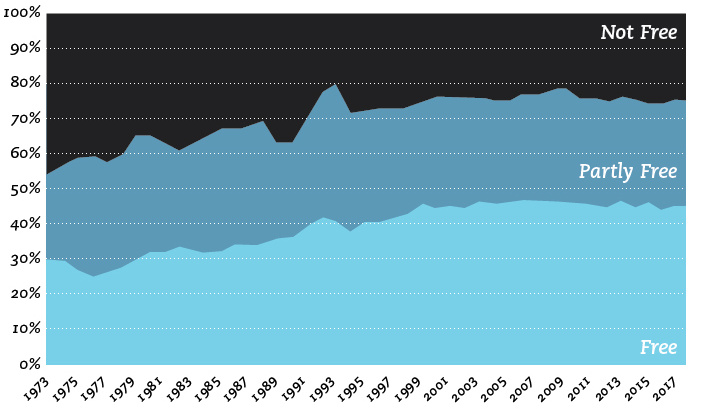

Freedom in the World, a report published every year since 1973, attempts to measure civil liberties and political rights around the world. It’s put together by Freedom House, a non-governmental organization based in the United States. According to their index, here is the share of “free” countries globally between 1973-2018:

This year’s report for 2018 is entitled “Democracy in Crisis”, and it sounds the alarm on eroding freedom throughout the world.

Falling Scores

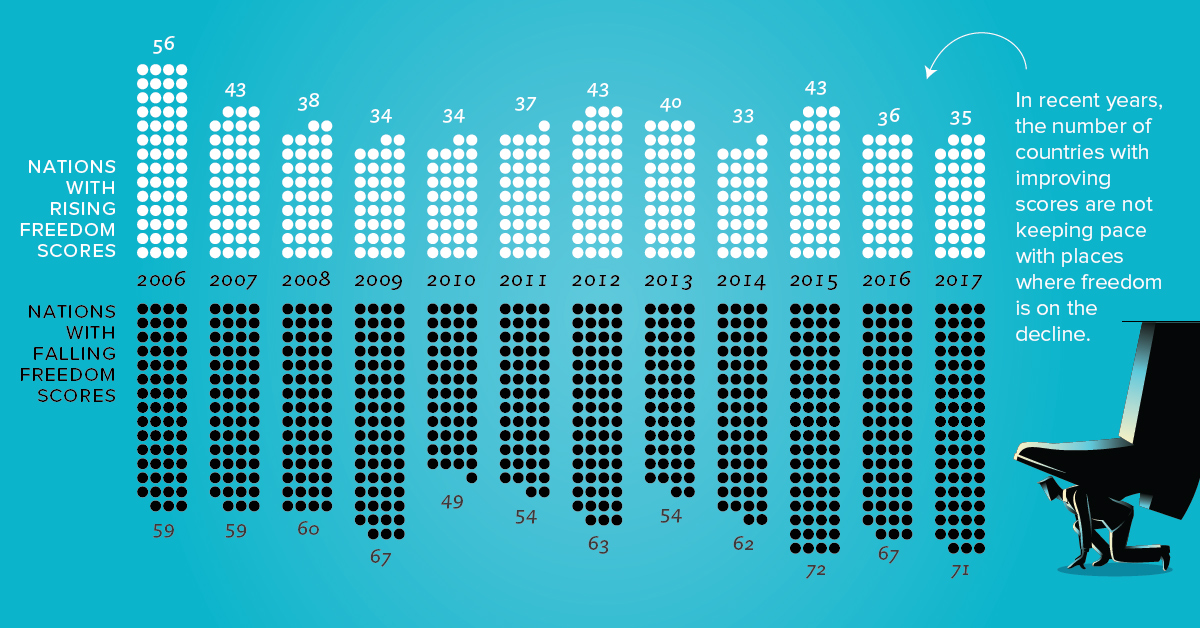

While the number of “free” countries is holding fairly steady at close to 45%, there is a clear downtrend with the scores of the countries themselves. In 2017, for example, there were 71 countries that had net declines in score, while only 35 had net increases. This makes for a differential of -36, which is the widest gap during the 12 year downtrend. Why do scores continue to decline? Here are some of the specific examples, cited by the report:

The erosion of democratic norms in the U.S., which is actually the extension of a seven year trend The expansion of influence from key autocracies, particularly Russia and China Turkey’s transition from “Partly Free” to “Not Free” – the result of President Erdoğan asserting more control over the country Big drops in the scores of European countries like Poland and Hungary, where populist leaders are consolidating power Another drop in Venezuela’s score, as the country undergoes a full-blown humanitarian crisis A recent backslide in the scores in Arab Spring countries – even in Tunisia, which was heralded as a democratic success story

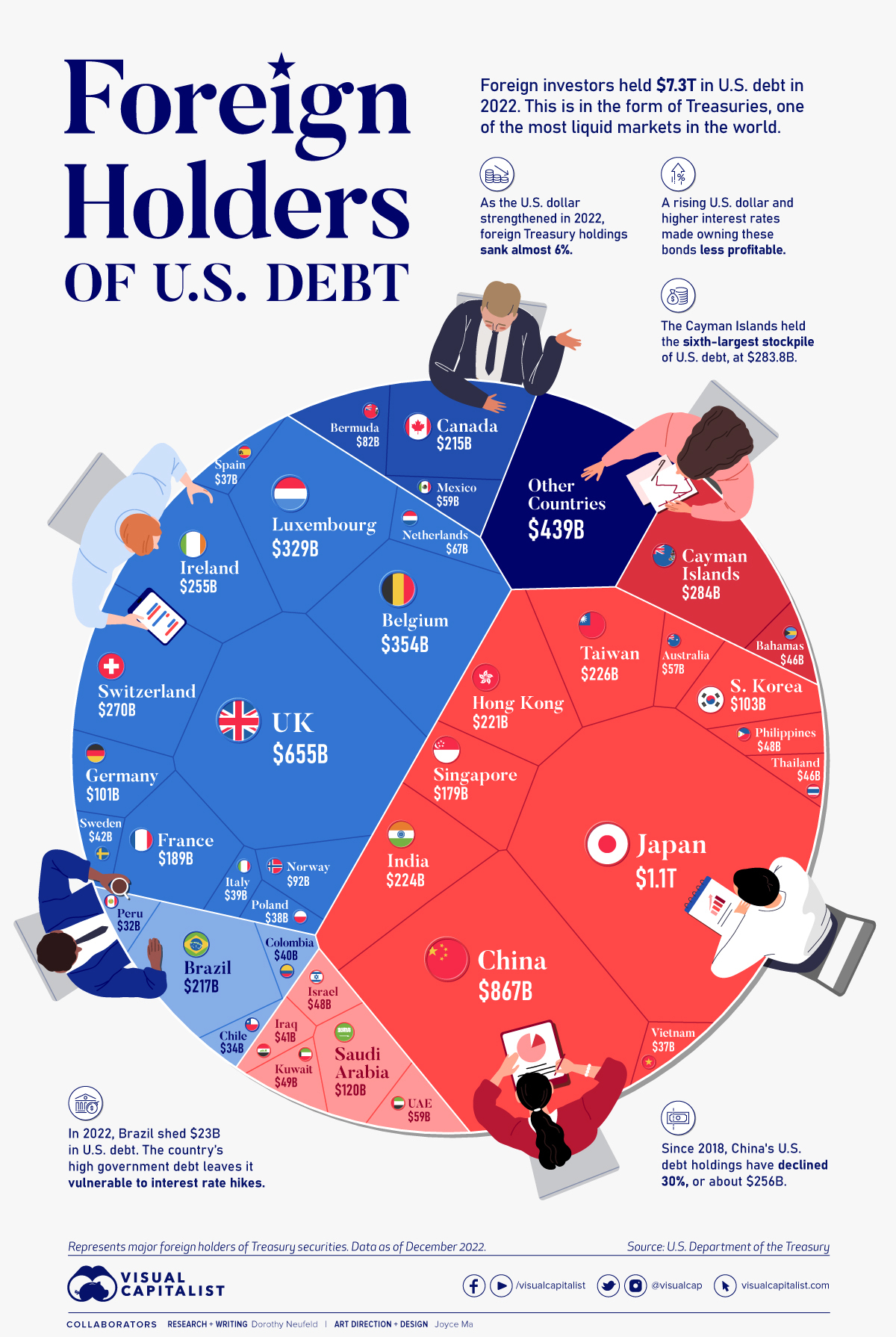

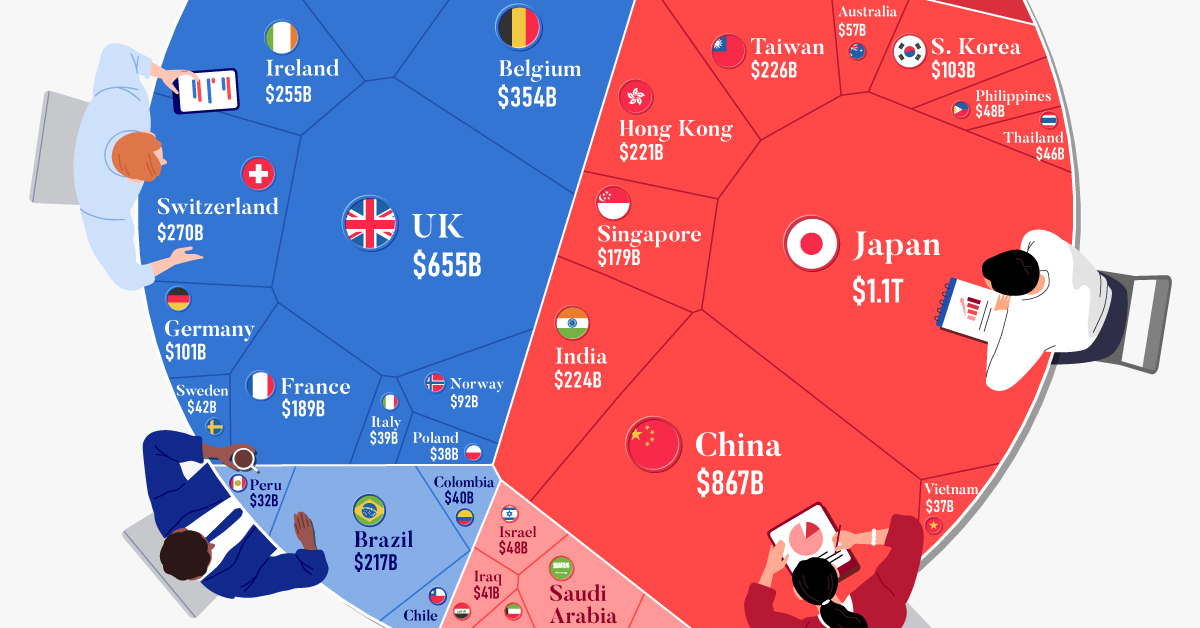

For much more in-depth reading, here is a link to the full report PDF. on These are in the form of Treasury securities, some of the most liquid assets worldwide. Central banks use them for foreign exchange reserves and private investors flock to them during flights to safety thanks to their perceived low default risk. Beyond these reasons, foreign investors may buy Treasuries as a store of value. They are often used as collateral during certain international trade transactions, or countries can use them to help manage exchange rate policy. For example, countries may buy Treasuries to protect their currency’s exchange rate from speculation. In the above graphic, we show the foreign holders of the U.S. national debt using data from the U.S. Department of the Treasury.

Top Foreign Holders of U.S. Debt

With $1.1 trillion in Treasury holdings, Japan is the largest foreign holder of U.S. debt. Japan surpassed China as the top holder in 2019 as China shed over $250 billion, or 30% of its holdings in four years. This bond offloading by China is the one way the country can manage the yuan’s exchange rate. This is because if it sells dollars, it can buy the yuan when the currency falls. At the same time, China doesn’t solely use the dollar to manage its currency—it now uses a basket of currencies. Here are the countries that hold the most U.S. debt: As the above table shows, the United Kingdom is the third highest holder, at over $655 billion in Treasuries. Across Europe, 13 countries are notable holders of these securities, the highest in any region, followed by Asia-Pacific at 11 different holders. A handful of small nations own a surprising amount of U.S. debt. With a population of 70,000, the Cayman Islands own a towering amount of Treasury bonds to the tune of $284 billion. There are more hedge funds domiciled in the Cayman Islands per capita than any other nation worldwide. In fact, the four smallest nations in the visualization above—Cayman Islands, Bermuda, Bahamas, and Luxembourg—have a combined population of just 1.2 million people, but own a staggering $741 billion in Treasuries.

Interest Rates and Treasury Market Dynamics

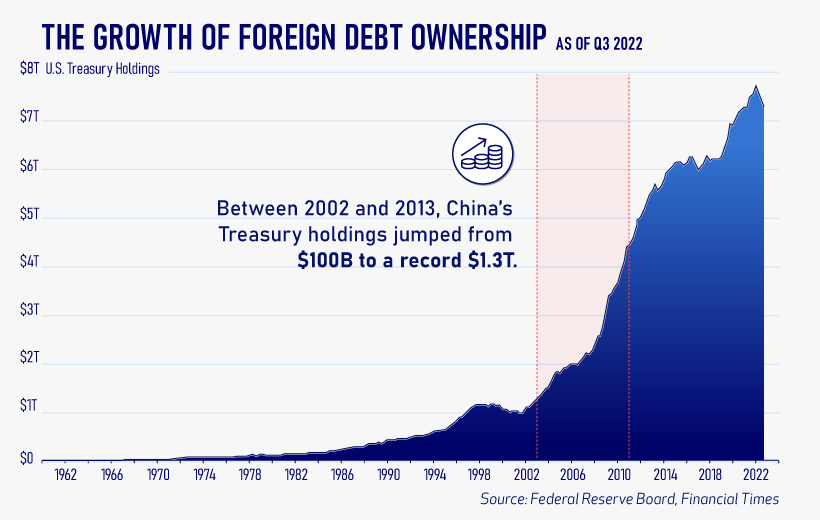

Over 2022, foreign demand for Treasuries sank 6% as higher interest rates and a strong U.S. dollar made owning these bonds less profitable. This is because rising interest rates on U.S. debt makes the present value of their future income payments lower. Meanwhile, their prices also fall. As the chart below shows, this drop in demand is a sharp reversal from 2018-2020, when demand jumped as interest rates hovered at historic lows. A similar trend took place in the decade after the 2008-09 financial crisis when U.S. debt holdings effectively tripled from $2 to $6 trillion.

Driving this trend was China’s rapid purchase of Treasuries, which ballooned from $100 billion in 2002 to a peak of $1.3 trillion in 2013. As the country’s exports and output expanded, it sold yuan and bought dollars to help alleviate exchange rate pressure on its currency. Fast-forward to today, and global interest-rate uncertainty—which in turn can impact national currency valuations and therefore demand for Treasuries—continues to be a factor impacting the future direction of foreign U.S. debt holdings.